Part 2) Red Sea Crisis: The Financial Ripple Effect

Following the initial security disruptions outlined in Part 1, the Red Sea crisis rapidly transformed into a significant financial shock. By forcing the world’s largest shipping lines to reroute vessels away from the Suez Canal, the situation disrupted global logistics, inflated operational costs, and pressured supply chains from the manufacturing floor to the retail shelf.

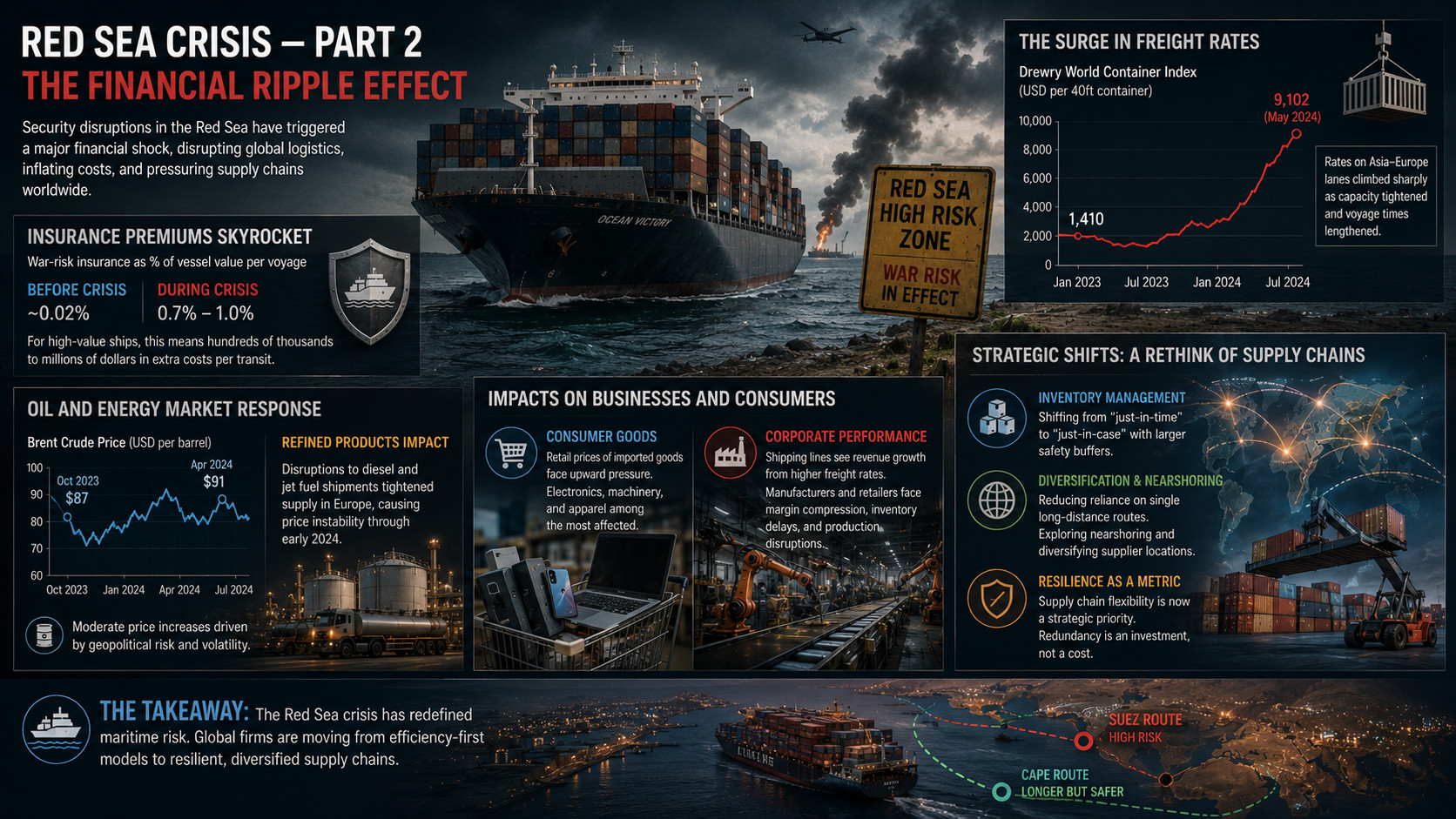

Red Sea Crisis — Part 2: The Financial Ripple Effect

Following the initial security disruptions outlined in Part 1, the Red Sea crisis rapidly transformed into a significant financial shock. By forcing the world’s largest shipping lines to reroute vessels away from the Suez Canal, the situation disrupted global logistics, inflated operational costs, and pressured supply chains from the manufacturing floor to the retail shelf.

The Surge in Freight Rates and Insurance

The most immediate consequence of the crisis was a dramatic increase in maritime logistics costs.

- Freight Indices: Global container freight rates saw a massive spike. The Drewry World Container Index, which tracks shipping costs, surged significantly between late 2023 and mid-2024. On major trade lanes—most notably those connecting Asia to Europe—rates climbed sharply as capacity tightened and voyage times lengthened.

- Insurance Premiums: The risk profile for transiting the Red Sea fundamentally changed. Once-negligible war-risk insurance premiums skyrocketed, with some reports indicating they rose to between 0.7% and 1% of a vessel's total value per voyage. For high-value ships, this translated into hundreds of thousands, sometimes millions, of dollars in additional expenses per transit.

The Oil and Energy Market Response

While crude oil flows faced disruption, the impact on energy markets was characterized more by risk-based volatility than by a total physical supply collapse.

- Pricing Pressure: Brent Crude prices initially reacted to the heightened geopolitical risk with moderate increases. However, the most acute energy impact was felt in the refined products market. Disruptions to the shipment of diesel and jet fuel from Middle Eastern and Asian refineries toward Europe tightened supply in the latter, contributing to price instability for European fuel markets throughout early 2024.

Impacts on Businesses and Consumers

The increase in shipping and insurance costs inevitably filtered through to the broader economy, though often with a 3–6 month lag:

- Consumer Goods: Retail prices for imported goods—particularly electronics, machinery, and apparel—faced upward pressure as companies sought to pass on higher logistics costs.

- Corporate Performance: The financial outcomes were bifurcated. Large shipping lines often saw revenue growth due to the elevated freight environment. In contrast, manufacturers and retailers, especially those reliant on "just-in-time" supply chains from Asia, faced margin compression, inventory delays, and the challenge of managing production shutdowns due to missing components.

Strategic Shifts: A Rethink of Supply Chains

The persistence of the security threat necessitated a move away from the efficiency-first models that defined global trade for decades. To build resilience against future chokepoint disruptions, corporations have begun to implement several strategic changes:

- Inventory Management: Shifting from "just-in-time" to "just-in-case" inventory models, maintaining larger safety buffers to absorb delivery delays.

- Diversification and Nearshoring: Reducing dependency on single, long-distance corridors by exploring nearshoring—moving production closer to end-consumer markets—and diversifying the geographic locations of key suppliers.

- Resilience as a Metric: Companies are increasingly prioritizing supply chain flexibility, treating logistical redundancy as a necessary investment rather than a cost to be eliminated.

This crisis has fundamentally changed how global firms perceive maritime risks, marking a transition toward a more cautious and diversified era of international trade.