Part 3) The Red Sea Crisis: A Stress Test for India’s Economy

The bottleneck in the Red Sea–Suez artery has introduced a fresh layer of strain on India's economy, driving up freight costs, adding an estimated $1–2 billion to the import bill, and impacting vital refining and manufacturing networks.

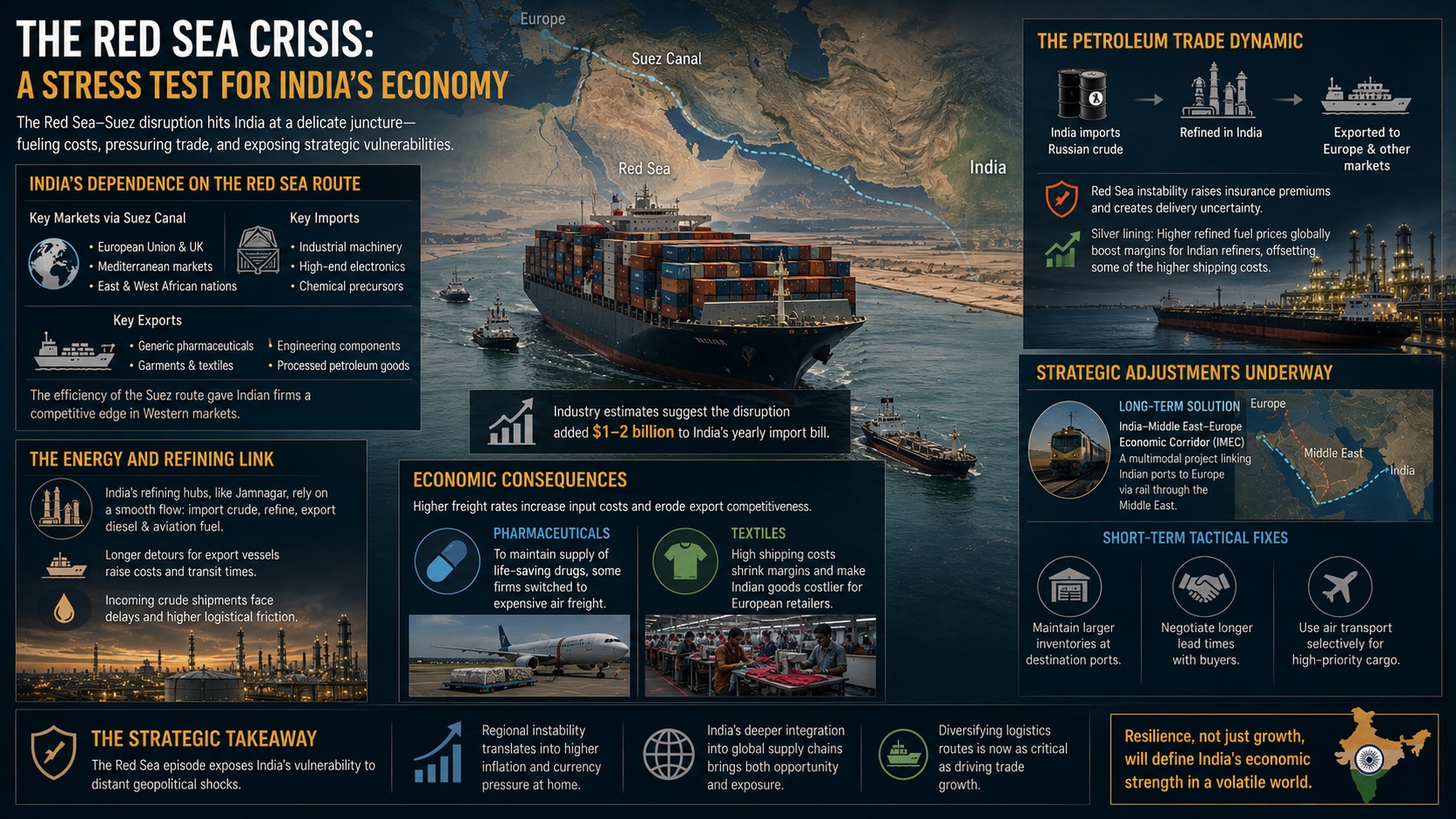

The Red Sea Crisis: A Stress Test for India’s Economy

For India, the volatility in the Red Sea arrived at a delicate juncture. The nation was already navigating sticky inflation, a fluctuating rupee, and a current account deficit highly sensitive to import pricing. The bottleneck in the Red Sea–Suez artery introduced a fresh layer of strain on an economy deeply tied to global maritime corridors.

India’s reliance on this passage extends beyond simple trade with Europe and Africa; it is a vital component of the country’s massive refining and manufacturing networks.

India’s Dependence on the Red Sea Route

A substantial volume of India’s commerce with the following regions passes through the Suez Canal:

- The European Union and the UK

- Mediterranean markets

- East and West African nations

Imports via this route primarily consist of industrial machinery, high-end electronics, and essential chemical precursors. On the export side, the corridor is indispensable for:

- Generic pharmaceuticals

- Garments and textiles

- Engineering components

- Processed petroleum goods

Historically, the efficiency of the Suez route provided Indian firms a competitive edge in Western markets by minimizing both transit times and logistics overheads.

The Energy and Refining Link

India’s status as a global refining powerhouse created a specific vulnerability. Major hubs, such as the Jamnagar refinery, rely on a seamless flow where crude is imported, processed, and then re-exported as diesel or aviation fuel. The crisis hampered this cycle by:

- Forcing export vessels onto longer, costlier detours.

- Introducing logistical friction for incoming crude shipments.

Economic Consequences

The financial impact filtered through the economy via several channels. Increased freight rates drove up the cost of raw materials while eroding the price competitiveness of Indian exports. Industry data suggests the disruption added an estimated $1–2 billion to India’s yearly import bill.

Specific sectors felt the pinch more acutely:

- Pharmaceuticals: To maintain global supply chains for life-saving drugs, some firms switched to expensive air freight.

- Textiles: Manufacturers faced shrinking margins as high shipping costs made their goods more expensive for European retailers.

The Petroleum Trade Dynamic

The energy sector faced a unique challenge. Following the shift in global geopolitics, India became a major buyer of Russian crude. Much of this oil is refined locally and shipped to Europe. The Red Sea instability increased insurance premiums and created significant delivery uncertainty.

However, there was a minor silver lining: as global shipping tightened, refined fuel prices rose, which helped bolster the margins for Indian refiners despite the surge in transportation costs.

Strategic Adjustments

The crisis accelerated India’s pursuit of alternative infrastructure to bypass maritime chokepoints. A key focus remains the India–Middle East–Europe Economic Corridor (IMEC), a multimodal project designed to link Indian ports to Europe via rail through the Middle East.

In the immediate term, businesses have turned to tactical fixes:

- Maintaining larger inventories at destination ports.

- Negotiating longer lead times with buyers.

- Selective use of air transport for high-priority shipments.

The Strategic Takeaway

The Red Sea episode serves as a reminder of India’s exposure to distant geopolitical shocks. As India integrates further into the global supply chain, it becomes more susceptible to disruptions in waters it does not control. This crisis proves that regional instability can lead directly to domestic inflation and currency pressure. For India, the future goal is not just trade growth, but building a more resilient, diversified logistics framework.